Buying a Home

Did Michigan Mortgage Rates Blast Off in 2022?

If you listen to the news, you will get fed consistent updates about how mortgage rates are jumping and how…

Articles on mortgage rates from the Riverbank Finance mortgage team.

If you listen to the news, you will get fed consistent updates about how mortgage rates are jumping and how…

Fannie Mae has announce that they will be raising rates on second home loan for all purchases after April 1st,…

It is our goal to educate our clients and advise them on the best options for home loans. The purpose…

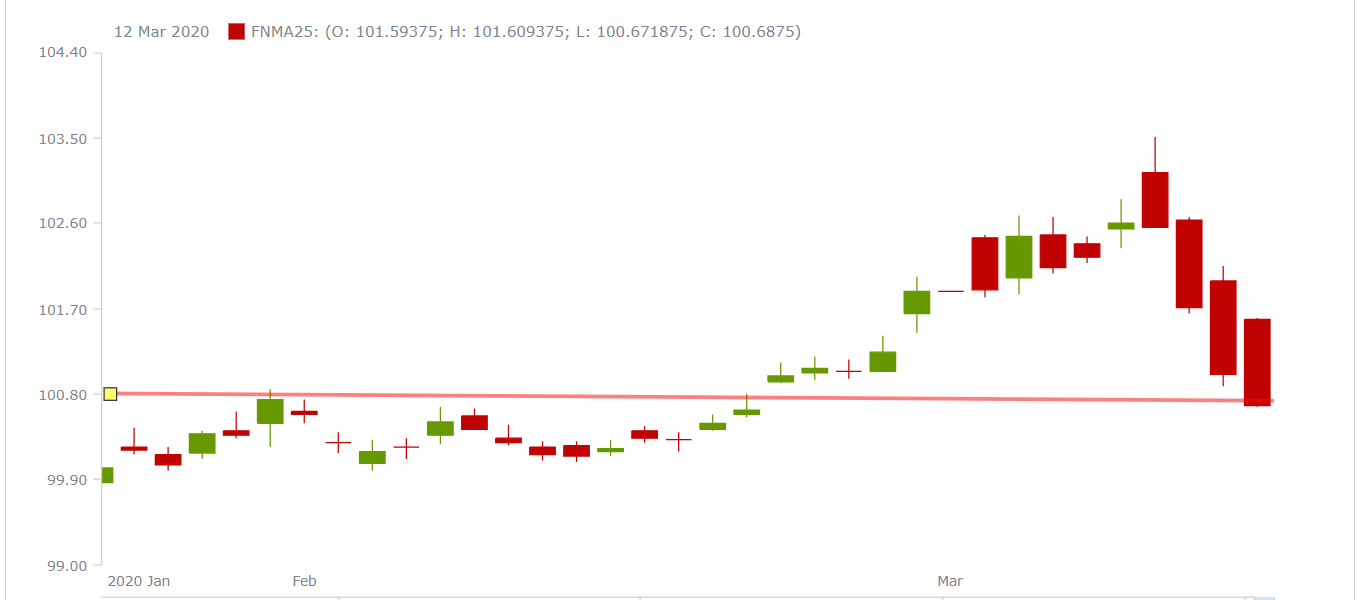

The Coronavirus has wreaked havoc on the financial markets so far in March 2020. Investors have been fleeing from stocks…

A brand new FICO credit scoring model will be used in the summer of 2020. These credit changes will affect…

March 2019 was the best month for Michigan Mortgage Rates in a Decade! Refinance your mortgage and Lock in a…

I know what you’re thinking: Why would I ever want to get an Adjustable Rate Mortgage? Isn’t it too risky?…

7 Mortgage Myths Debunked It is no secret that the home buying process is a long and complicated one. Getting…

Apply online in about 15 minutes, or talk to a licensed loan officer today. No pressure — just straight answers and low rates.

Apply Now 800-555-2098