Local Michigan

Mortgage Broker Lending Partner UWM Goes Public

Today is an exciting day for independent mortgage brokers! Our #1 lending partner United Wholesale Mortgage (UWM) completed their IPO…

Articles on mortgage broker from the Riverbank Finance mortgage team.

Today is an exciting day for independent mortgage brokers! Our #1 lending partner United Wholesale Mortgage (UWM) completed their IPO…

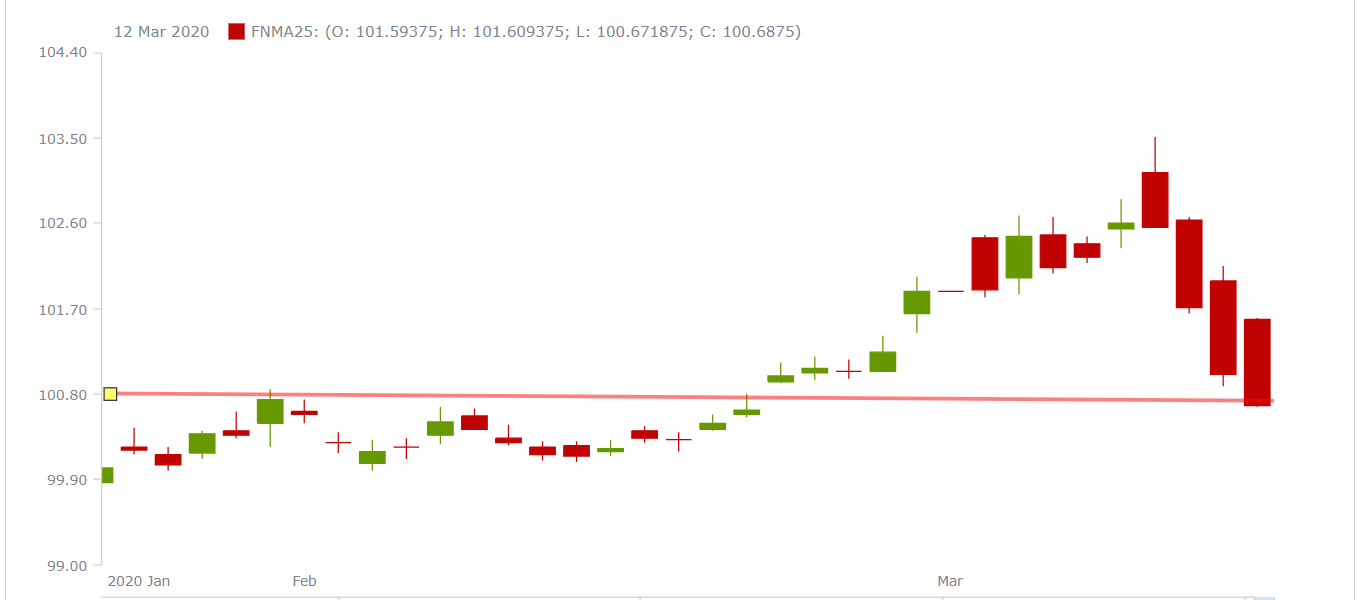

The Coronavirus has wreaked havoc on the financial markets so far in March 2020. Investors have been fleeing from stocks…

Mortgage Broker Growth What is a Mortgage Broker? Mortgage Broker Benefits Loan Support Transparency on Rates and Fees Loan…

You may have heard that the Federal Reserve has been cutting rates to slow economic slowdown. Industry experts predict that…

Mortgage Broker Myth #1 One of the biggest myths of using a Mortgage Broker is that they do not have…

Bankers and Lenders and Brokers, Oh My! Mortgage Bankers When many prospective homebuyers think about getting pre-approved for a mortgage,…

Many people have the misconception that to qualify for the Home Affordable Refinance Program they must contact their current servicer…

Apply online in about 15 minutes, or talk to a licensed loan officer today. No pressure — just straight answers and low rates.

Apply Now 800-555-2098