You may have heard some buzz this spring about mortgage giant Fannie Mae and trended credit data, changes which were set to take effect in June. Just days before the launch, however, the new system was delayed unexpectedly. Well folks, long-awaited Desktop Underwriter 10.0 launched this past weekend, and with it, the requirement that lenders use trended credit data on all new loan casefiles.

What is Trended Credit Data?

Trended credit data is a detailed record of credit history, including payment history and total balance each month. The addition of this new information will allow lenders to more accurately tell the difference between ‘transactors’—borrowers with large balances who pay in full each month—and ‘revolvers’—borrowers with large balances who pay only the minimum payment each month. Until now, existing credit reports could not distinguish the two.

The new credit report will feature trended credit data history on credit cards, HELOCs, student loans, car loans, and mortgages. The actual appearance of credit reports will change very little, but will include 30 months’ history with Transunion and 24 months’ history with Equifax; Experian plans to add trended credit data in January 2017. Neither FICO or VantageScores incorporate trended data into their system at this time.

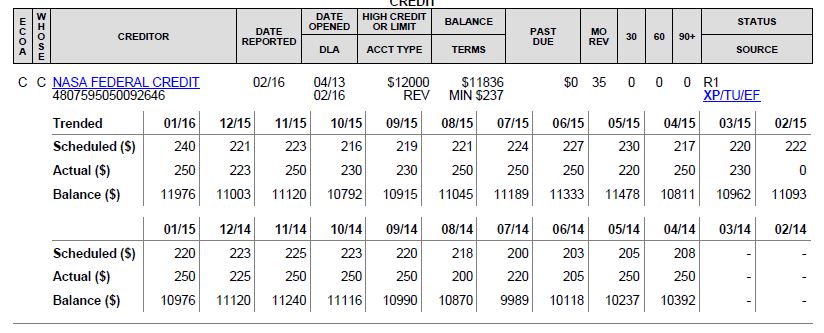

The example above shows a revolving account with trended credit data.

Why is This Important?

The addition of trended credit data provides a more detailed picture of a borrower’s credit behavior, rather than the traditional moment-in-time credit snapshot. It allows lenders to better predict your future payment behavior and assess your risk.

“The trended credit data will be used by the DU risk assessment to evaluate how the borrower manages his/her revolving credit card accounts. A borrower who uses revolving accounts conservatively (low revolving credit utilization and/or regular payoff of revolving balance) will be considered a lower risk. A borrower whose revolving credit utilization is high and/or who makes only the minimum monthly payment each month will be considered higher risk.” – Fannie Mae

How will this affect my credit score?

Fannie Mae has not yet released conclusive guidelines as to how trended data will be scored or impact the underwriting process. Financial institutions across the country, however, speculate that this will open up the credit window to potential borrowers previously deemed unworthy. That’s right—trended credit data can turn a denial into an approval!

Even the most responsible borrowers make mistakes, but forgetting to make a payment will cost you more than just a large late fee—it can lower your credit score upwards of 100 points, in some cases! Until now, only years of hard work and waiting for delinquencies to season could rebound a credit score. With the addition of trended data, however, a borrower can effectively counter that late payment within a couple of months. Tendencies such as paying off revolving balances in full, making additional payments, and reducing total amount borrowed over time all demonstrate positive repayment ability and behavior.

Have a specific scenario you’d like to run past us? Give us a call to speak with one of our licensed loan officers. We would love to recommend the best loan program for you and your situation.

Apply for a Mortgage

Call Riverbank Finance today at 1-800-555-2098