800-555-2098

800-555-2098

Buying a home is often the largest purchase of your lifetime—but what if you could stretch your payments over half a century? Enter the 50 year mortgage: an increasingly popular solution for buyers hungry to lower monthly costs.

President Trump announces on Truth Social that he plans on implementing a 50 year mortgage. Lets review the 50 year mortgage and what it really means for a homeowner. We will cover the benefits and downsides, and help you decide if it’s the right home loan in 2025.

Also lets talk about how you can get best rates, requirements you can’t ignore, and smarter alternatives to consider. Ready to extend your amortization—and maybe your peace of mind?

What Is a 50 Year Mortgage?

Picture this: a mortgage that stretches five decades into the future. That’s what we’re talking about with a 50 year mortgage—we can call it a “half-century” loan.

Here’s the deal… while your typical 30-year mortgage spreads payments over three decades, a 50 year loan gives you two extra decades to pay it off. Think of it like choosing between a sprint and a marathon. The marathon (50 year) gives you a slower, steadier pace.

The math is pretty straightforward. Take a $400,000 home loan at 7% interest. With a 30-year mortgage, you’re looking at roughly $2,661 monthly. Stretch that same loan to 50 years? Your payment drops to about $2406. That’s over $250 in monthly savings.

But here’s where it gets interesting… 50 year mortgages aren’t exactly new. They popped up during the housing crisis when lenders got creative with affordability solutions. Now they’re making a comeback as home prices continue climbing faster than most people’s paychecks.

I remember when a colleague first mentioned these loans back in 2019. My initial reaction? “Fifty years? Who wants to be 85 and still making mortgage payments?” But after diving deeper into the numbers, I realized there’s more nuance here than meets the eye.

Who Benefits from a 50 Year Mortgage?

Let’s get real about who actually makes sense for these extended loans. If you can get a mortgage and pay it off in 30 years, why might you chose 50 years to repay?

First-time buyers feeling the squeeze. When you’re competing against cash offers and bidding wars, sometimes you need every advantage possible. Lower monthly payments can be the difference between qualifying for that dream home or staying stuck in rental purgatory.

Freelancers and gig workers. Your income bounces around like a ping-pong ball, but you still want homeownership stability. That extra breathing room each month can be a lifesaver when client payments run late or projects dry up. An extended mortgage term would give you lower monthly payments and help you qualify with less income.

Coastal market survivors. Try buying anything decent in San Francisco or Manhattan on a normal salary. Sometimes a 50 year mortgage is the only way to crack into these markets without selling a kidney. With housing pricing soaring, homebuyers are looking at all options to help keep payments affordable.

Strategic retirees. Here’s a curveball—some retirees use these loans to unlock home equity while keeping payments manageable on fixed incomes. It’s not always about buying your first home. If you get a mortgage when you are in your 70’s or 80’s, what is the difference between 30 years and 50 years?

Pros of a 50 Year Mortgage

Loan Term | 50-Year Mortgage | 30-Year Mortgage (for comparison) |

|---|---|---|

| Monthly Payments | Lower, potentially making homeownership more accessible. | Higher than a 50-year loan for the same principal. |

| Total Interest Paid | Significantly higher over the life of the loan (potentially double or more). | Lower total interest costs. |

| Equity Building | Very slow, especially in the initial years. | Faster equity accumulation. |

| Loan Term | Extends debt for a lifetime for many borrowers. | Standard term that is typically paid off or refinanced within 7-12 years. |

| Interest Rate | May come with a slightly higher interest rate due to increased risk for the lender. | Generally offers more competitive rates. |

The benefits hit you right in the wallet first; well at least on the monthly payments.

Cash flow becomes your friend. Those lower monthly payments free up serious money for other priorities. Maybe you can finally max out that 401(k) or build an emergency fund that actually covers emergencies.

Qualification gets easier. Lenders love seeing lower debt-to-income ratios. When your housing payment drops by $300-500 monthly, suddenly you look much more attractive on paper.

Investment opportunities open up. This is where things get spicy. Take that extra $400 monthly and invest it properly over 30 years… you might come out ahead even after paying more mortgage interest. It’s all about opportunity cost.

Budget flexibility rocks. Life throws curveballs. Job loss, medical bills, kids needing braces—having lower required payments gives you wiggle room when crisis hits.

I once worked with a young engineer who chose a 50 year mortgage specifically to invest the payment difference. Smart guy ran the numbers and figured the stock market would likely beat his mortgage rate over time. Risky? Maybe. But he had a solid plan and the discipline to execute it.

Cons and Trade-Offs of 50 Year Mortgages

Now for the reality check…

Interest costs will make you wince. That same $400,000 loan? You’ll pay roughly $1,044,000 in interest over 50 years versus $558,000 over 30 years. We’re talking nearly double the interest a homebuyer would pay to extend the loan for an additional 20 years.

Equity builds like molasses. For the first decade, you’re barely denting the principal balance. Your home needs to appreciate significantly just to break even if you need to sell early.

Negative amortization lurks. Some 50 year loans include payment caps that don’t even cover the interest. Your balance can actually grow over time. It’s like quicksand for your net worth.

Lender options stay limited. Most big banks don’t offer these loans. Usually they are more conservative and will only offer programs to serve the cream of the crop borrowers. Eventually if lenders start offering 50 year mortgages they could come with higher rates and fees compared to shorter term mortgages.

Interest Rates & Fees: What to Expect

Here’s the pricing reality for 2025…

50 year mortgages rates might run 0.25% to 0.75% higher than comparable 30-year rates. If 30-year fixed rates hover around 6.25%, expect 50 year rates between 6.75% and 7.00%.

Related: Calculate total interest paid with our mortgage amortization schedule calculator.

Your credit score matters more here. Excellent credit (740+) gets you the best pricing, while scores below 680 might face significant rate bumps or outright rejection.

Loan-to-value ratios may get scrutinized heavily. Some lenders may want 20% down minimum which may defeat the purpose of making homes affordable for first time homebuyers.

PMI may be impossible to get approved until the major insurance agencies roll out the insurance for these new mortgage programs. Once they are out, the PMI rates may be higher than a 30 year fixed mortgage rate.

Discount points work the same way—pay upfront to buy down your rate. But do the math carefully since you’re spreading that cost over five decades.

Closing costs should mirror traditional mortgages: origination fees, appraisal, title insurance, recording fees. Budget 1-3% of loan amount total.

Qualifying for a 50 Year Mortgage

The qualification bar sits higher than you might expect.

Credit scores need muscle. Most lenders want 680 minimum, with 720+ getting preferred pricing. Your credit report gets extra scrutiny since the extended term increases their risk.

Down payments start at 10%. Though 20% down remains the sweet spot for avoiding mortgage insurance and getting better rates.

Income documentation stays thorough. W-2 employees provide two years of tax returns plus recent pay stubs. Self-employed borrowers need comprehensive profit/loss statements and bank records.

Debt-to-income ratios get tight. Even with lower payments, many lenders cap DTI at 43% including your new mortgage payment.

Seasoning rules apply. Recent job changes, credit inquiries, or large deposits trigger additional documentation requirements.

Some lenders add their own overlays—maybe requiring larger cash reserves or restricting property types. It pays to shop around.

How to Apply for a 50 Year Mortgage

Shopping for a 50 year mortgage requires extra legwork since fewer lenders offer them. Working with an experience mortgage broker may have more options that the big banks.

Pre-qualification vs. pre-approval matters more here. Pre-qualification gives you a ballpark based on basic info. Pre-approval involves full documentation review and credit analysis—much more valuable when you’re dealing with specialized loan products.

The underwriting timeline typically runs 15-45 days, sometimes longer if your financial situation involves complexity. Self-employed borrowers should expect additional documentation requests.

Required paperwork includes: tax returns, pay stubs, bank statements, asset documentation, employment verification letters, and detailed explanations for any credit issues.

Closing day follows the standard script—final walkthrough, document signing, funding. Just be prepared for extra questions about your long-term payment strategy.

Comparing Alternatives: 30-Year, 40-Year & Hybrid Loans

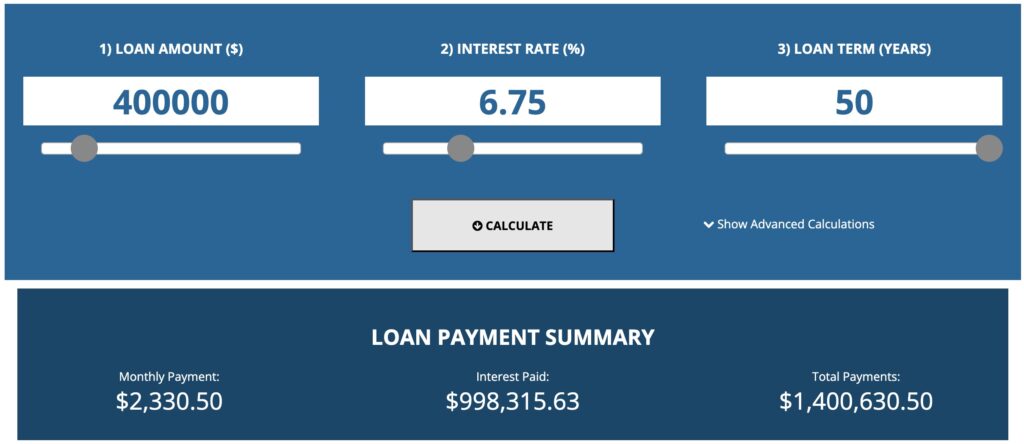

Let’s run some numbers on a $400,000 loan at current estimates rates… (Note: rates are for example purposes only. For a quote for your specific situation be sure to reach out to your loan officer or give us a call at 800-555-2098).

30-year fixed (6.25%): $2,462 monthly, $486,631 total interest

40-year fixed (6.50%): $2,341 monthly, $724,071 total interest

50 year fixed (6.75%): $2,330 monthly, $998,315 total interest

Notice the pattern? Each extra decade saves you roughly $10 monthly but costs $250,000+ in lifetime interest.

40-year mortgages offer middle ground—meaningful payment reduction without the extreme interest penalty of 50 year terms. More lenders offer them too.

Interest-only loans provide even lower initial payments but come with payment shock when the interest-only period ends. They’re risky unless you have solid appreciation expectations.

Adjustable-rate mortgages might start lower but introduce rate risk over time. With a 50 year term, you’re exposed to decades of potential rate increases.

A client once told me choosing between these options felt like picking between different types of expensive coffee. “They’re all pricey,” he said, “but some give you more bang for your buck.” Smart perspective.

Strategies to Pay Off Faster

Here’s the secret sauce… just because you have 50 years doesn’t mean you need to use all of them.

Biweekly payments work magic. Instead of 12 monthly payments yearly, make 26 biweekly payments (equivalent to 13 monthly payments). You’ll shave roughly 6-8 years off your loan term.

Windfall applications accelerate progress. Tax refunds, bonuses, inheritances—apply these directly to principal. Even $1,000 extra annually makes a huge difference over time.

Refinancing opportunities emerge. When rates drop significantly or your financial situation improves, refinance into shorter terms. The 50 year loan becomes a temporary affordability bridge.

Mortgage accelerator apps help automate extra payments. Some round up purchases and apply spare change to your mortgage principal. It sounds gimmicky but adds up over time.

If a couple who takes a 50 year mortgage but committed to paying it off in 25 years through extra payments. If they want the flexibility of lower required payments but the discipline of faster payoff. Best of both worlds.

Common Questions & Pain Points

“Will my appraisal reflect my home’s true value?”

Appraisals work the same regardless of loan term. However, some appraisers might be extra conservative knowing you’re using non-traditional financing. Consider getting a pre-listing appraisal to avoid surprises.

“Can I refinance out of a 50 year loan?”

Absolutely. You can refinance anytime, subject to normal qualification requirements. Many borrowers might use 50 year loans as temporary affordability solutions while building equity and improving credit. Once they earn more income they could refinance to lower rates an a 30 year fixed rate mortgage or even a 15 year fixed rate mortgage.

“How can I save the most amount of interest on a mortgage?”

Utilizing a shorter term mortgage like a 10 year loan or even a 15 year fixed rate mortgage will allow you to save thousands of dollars of interest compared to longer terms.

“What happens if I sell before year 50?”

You pay off the remaining balance like any mortgage. The concern is slow equity buildup—you might owe more than expected if home appreciation doesn’t keep pace.

“Is it harder to qualify than a 30-year mortgage?”

Possibly. Lenders may impose stricter requirements because extended terms increase their risk. Higher credit scores, larger down payments, and lower debt ratios might be common requirements.

The biggest pain point I hear? Finding lenders who actually offer these loans. It takes patience and persistence to shop effectively in this limited market. A mortgage broker may be your best solution to find 50 year mortgage.

Is a 50 Year Mortgage a good idea?

A 50 year mortgage can unlock lower monthly payments and improved cash flow—but it’s not for everyone. You’ll trade decades of interest costs and slower equity gains for immediate budget relief. Before you commit, weigh the long-term implications, shop multiple lenders, and crunch the numbers on total interest paid.

Ready to explore whether a 50 year mortgage suits your financial plan? Reach out to a qualified mortgage advisor today, request personalized quotes, and take control of your home-buying journey in 2025!