Buying a Home

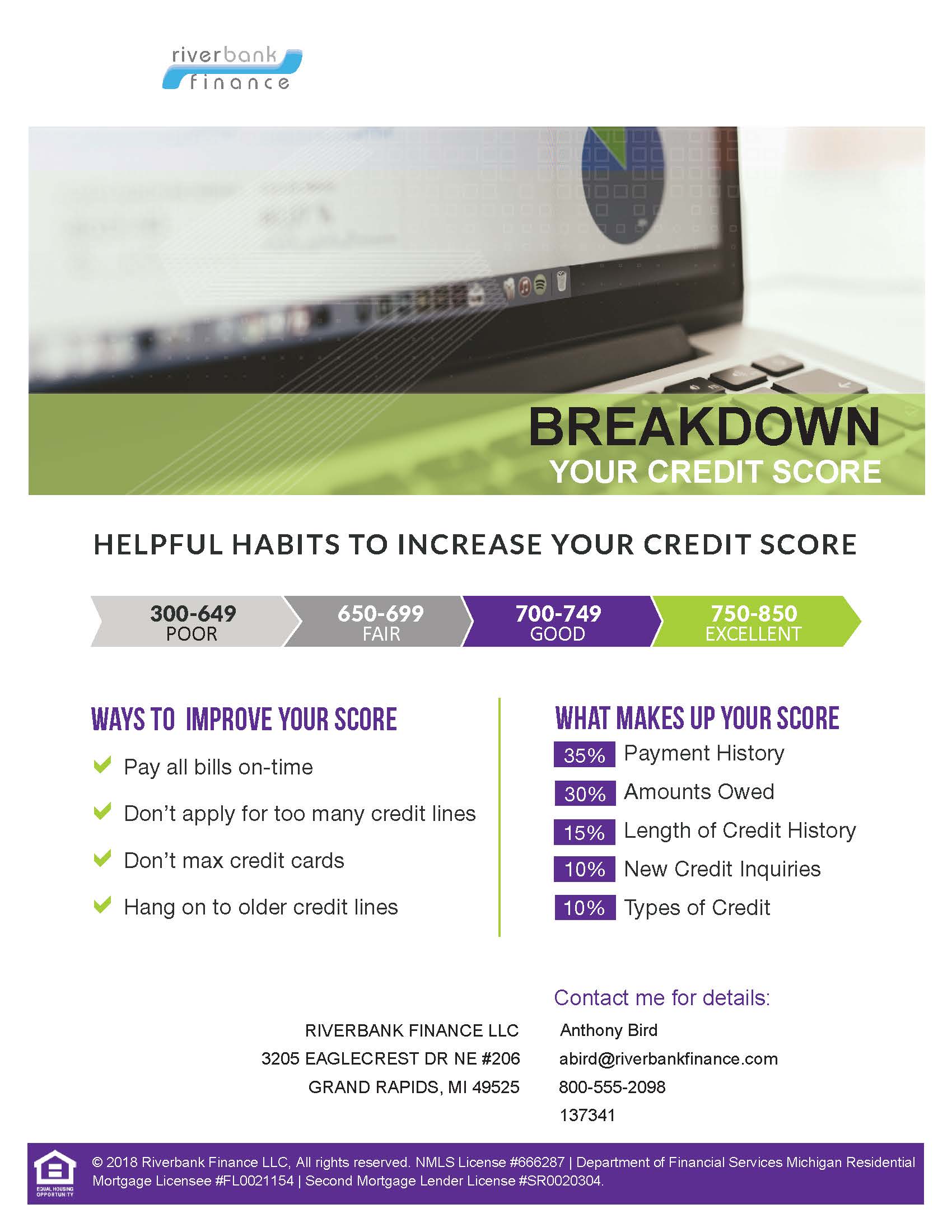

Breakdown Your Credit Score

When buying a home, your credit score is an important factor in your home loan approval. It is important to…

Articles on improve credit from the Riverbank Finance mortgage team.

When buying a home, your credit score is an important factor in your home loan approval. It is important to…

The History of Credit Scores Credit reports and scores have played a large part in many Americans’ lives, but what…

Mortgages have been a hot topic of conversation lately as rates continue to track lower and lower. People continue to…

Apply online in about 15 minutes, or talk to a licensed loan officer today. No pressure — just straight answers and low rates.

Apply Now 800-555-2098