Buying a Home

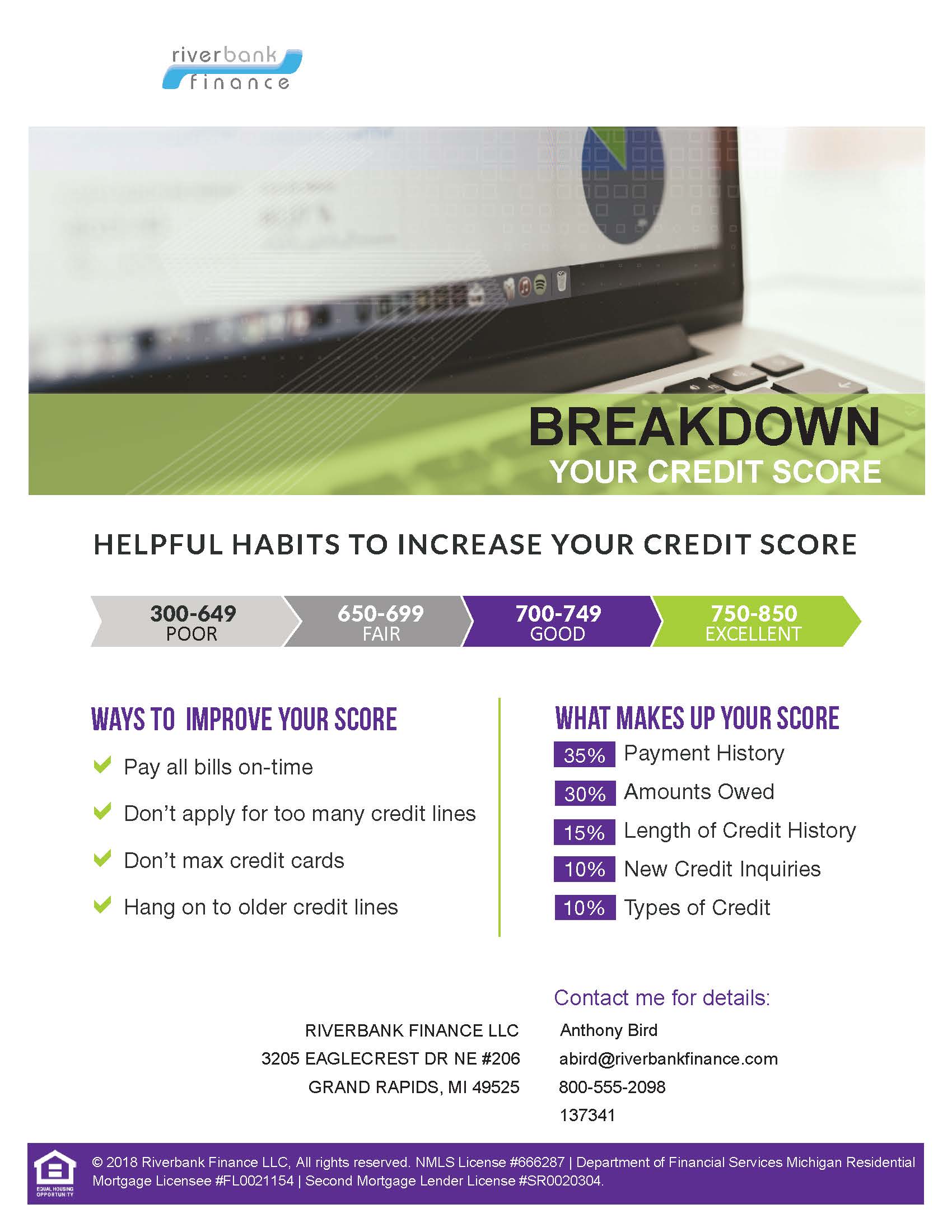

Breakdown Your Credit Score

When buying a home, your credit score is an important factor in your home loan approval. It is important to…

Articles on credit score from the Riverbank Finance mortgage team.

When buying a home, your credit score is an important factor in your home loan approval. It is important to…

While it can be useful to listen to the advice from others who have gotten a mortgage, you might have…

The process of getting a home loan when self-employed does not have to be difficult if you are prepared. While the…

You may have heard some buzz this spring about mortgage giant Fannie Mae and trended credit data, changes which were…

Apply online in about 15 minutes, or talk to a licensed loan officer today. No pressure — just straight answers and low rates.

Apply Now 800-555-2098