When it comes to home loans, there are hundreds of loan programs and options that you may want to consider. Many first time home buyers do not know where to start when they want to buy a home. It is overwhelming to most people who do not have experience buying a home or getting a mortgage. The good news is, a loan officer can be your tour guide to help you get the best mortgage loan.

When it comes to home loans, there are hundreds of loan programs and options that you may want to consider. Many first time home buyers do not know where to start when they want to buy a home. It is overwhelming to most people who do not have experience buying a home or getting a mortgage. The good news is, a loan officer can be your tour guide to help you get the best mortgage loan.

A loan officer’s job is to review your financial situation and provide home loan options. They will help to narrow down mortgage programs that do not fit your goals and also ones that you may not be eligible for. Here are the basic categories that you should review with your loan officer to get the best mortgage for your situation.

What Mortgage Program is the Best?

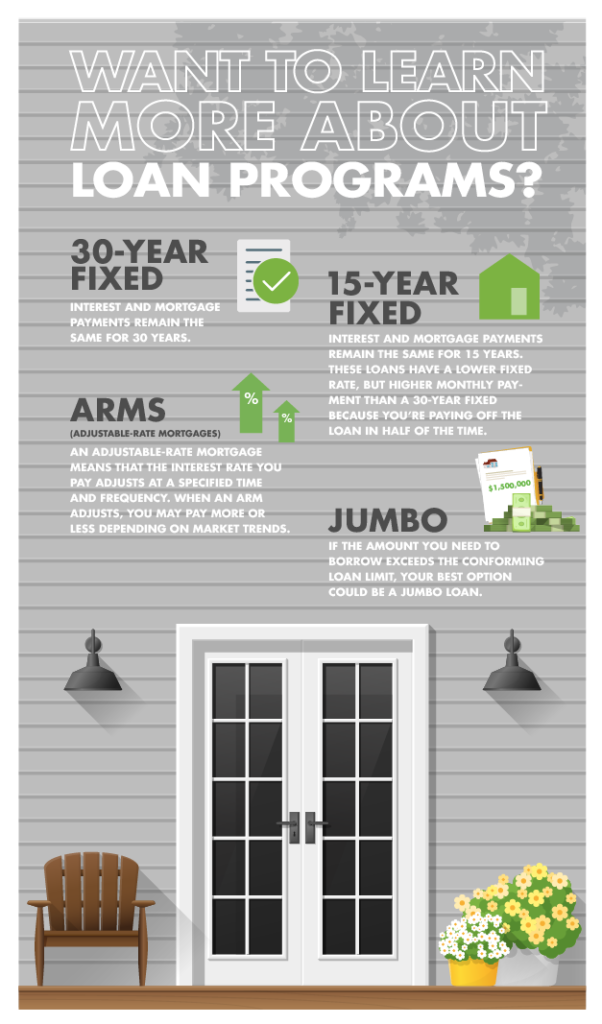

There are several loan programs that you can apply for including Conventional Loans, FHA Loans, VA Loans, USDA Rural Development Loans, Jumbo loans, and Portfolio Loans. Each loan program has its pros and cons.

Related: Conventional Loan vs FHA Loan vs VA Loan vs USDA Home Loans

You may not be eligible for some programs. VA Loans, for example, require that you have served in the military. If you haven’t served, then this would not be a loan option for you. Conventional loans typically require higher credit scores and are more rate sensitive to lower credit scores. USDA RD Loans, have income limits and restricted areas where you can purchase.

As you can see it is nearly impossible to quickly learn all the ins and outs of each program when you are buying a home. A loan officer can help offer options on what loan program may be the best fit for your situation.

What Mortgage Term is the Best?

Once you decide on what mortgage program will be the best fit for your situation, you will need to decide on a mortgage term. Loan terms range anywhere from 10 years to 40 years for some programs. For most loan programs we could even offer a 17 year loan or a 27 year mortgage based on your goals. The most popular mortgage option is a 30 year mortgage.

Many financial advisers recommend a 15 year fixed rate mortgage. This allows you to get a great rate and pay off your mortgage quickly. Typically loan rates are lower for shorter term loans. The downside is that the monthly payment will be higher the shorter your loan term is.

A traditional 30 year mortgage term has low payments but most of the payment goes directly to interest for the first several years. Many people are shocked at how little their loan balance goes down after a year or two of mortgage payments.

Be sure to ask your loan officer what mortgage term is best for your goals.

Include Escrows or Waive Escrows?

When you get a mortgage you may have the option to include escrows into your mortgage payment. An escrow account is a savings account held for you by your mortgage servicer that is specifically for paying the property taxes and home owners insurance on your home.

Typically, government insured mortgages including FHA, VA and USDA require you to have an escrow account included with your mortgage.

Conventional loans may allow you to waive escrows. This means that you would be responsible to pay your own taxes and home owners insurance bills when they become due.

Many people like escrow accounts for the ease of payment. It is one less thing homeowners need to worry about when buying a home. On the other hand, some people would rather waive escrows and keep their own savings where they can earn interest and be more in control of their funds.

Fixed Rate or Adjustable Rate?

A major choice to consider when getting a mortgage is if you would rather have a fixed rate or an adjustable rate. Most homeowners choose to have a fixed rate that does not change for the life of your loan. This gives predictable payments and certainty that your payment will not adjust.

Other homeowners wish to choose an adjustable rate mortgage, commonly refereed to as an ARM Loan. Typically ARMs start off with a lower rate which is locked for a set number of years (3, 5, 7, or 10 years). Once the initial fixed period is up, the rates are subject to adjustments to the LIBOR or other indexes. If the rates go up, your mortgage payment goes up. If the rates go down, your mortgage payment goes down.

Choosing a fixed rate is thought to be a more safe and secure loan option. ARMs should be carefully considered for financially savvy homeowners. Be sure to ask your loan officer about ARM Loans if you are interested otherwise a fixed rate mortgage is most likely the best choice.

What Interest Rate Should I Pick?

Lastly, when getting a mortgage, you have to pick a mortgage rate. Many people do not realized that they have options for different mortgage rates. Once you select all of your other mortgage details, your loan officer will present your mortgage rate options.

When it comes to mortgage rates, you also need to consider the fees associated with getting the loan. Typically, the lower the rate, the higher the fee. Conversely, the higher the rate, the lower the fees.

Should I Pay Discount Points?

If you want the lowest rate possible, you can certainly request a rock bottom interest rate but be prepared to pay discount points for a rate lower than the market rates.

If you want to make sure you are having the lowest costs to get a mortgage, then you may want to consider a slightly higher interest rate. Picking a higher rate may allow you to have no lender fee or even receive a lender credit that will apply towards other closing costs and pre-paid items like taxes and insurances.

Deciding what rate and fee combination can seem difficult, but your loan officer can help you do a break even analysis to compare the time to break even on your investment of paying points for lower rates.

Lets look at an example: If you were to pay 2 points on a $100,000 loan for a lower rate, this would cost you $2,000 in extra closing costs. By getting the lower rate, lets say you save $50 per month.

To find your break even point, you will divide your extra costs of $2,000 by your savings of $50 which would give you 40 months, or 3.33 years to break even on your up front investment.

If you plan on staying in the house for 5 years, then you will save more than your costs therefore paying points may make sense. If you plan on selling your home in 2 years, then you would not benefit from the up front investment and you would be better off taking the higher rate with lower fees.

There are many factors to consider to get the best mortgage for your situation. It is not as easy as simply picking the lowest rate. Be sure to work with a trusted loan officer that can help review all the mortgage programs to get you the best mortgage for your situation.

For more information on home loan programs or to review the best loan for you, request information below or call a loan officer at 800-555-2098.