U.S. homeowners are sitting on roughly $34.5 trillion in home equity right now. That’s a record. And with mortgage rates still holding above 6%, almost nobody wants to give up a 3% rate they locked in a few years ago just to pull out cash.

So homeowners are turning to home equity products instead — borrowing against what they’ve built without touching their first mortgage. Two products dominate that space: the HELOC and the home equity loan (HELOAN). They both tap your equity. They both sit behind your existing mortgage. But they work very differently, and picking the wrong one can cost you real money.

This guide breaks down the HELOC vs. home equity loan decision completely — how each works, what rates look like right now, and a simple framework for choosing the right one for your situation.

How a HELOC works

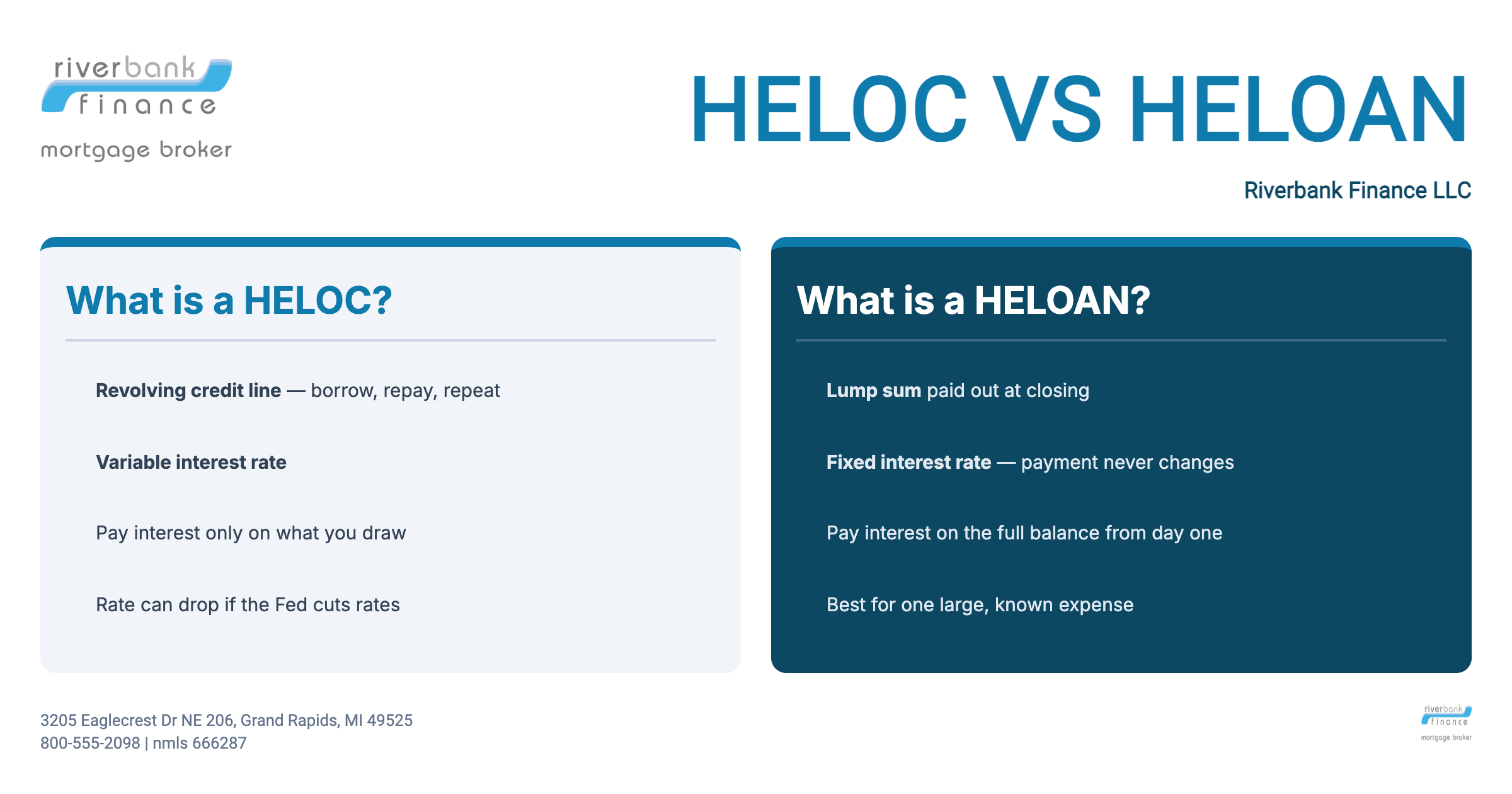

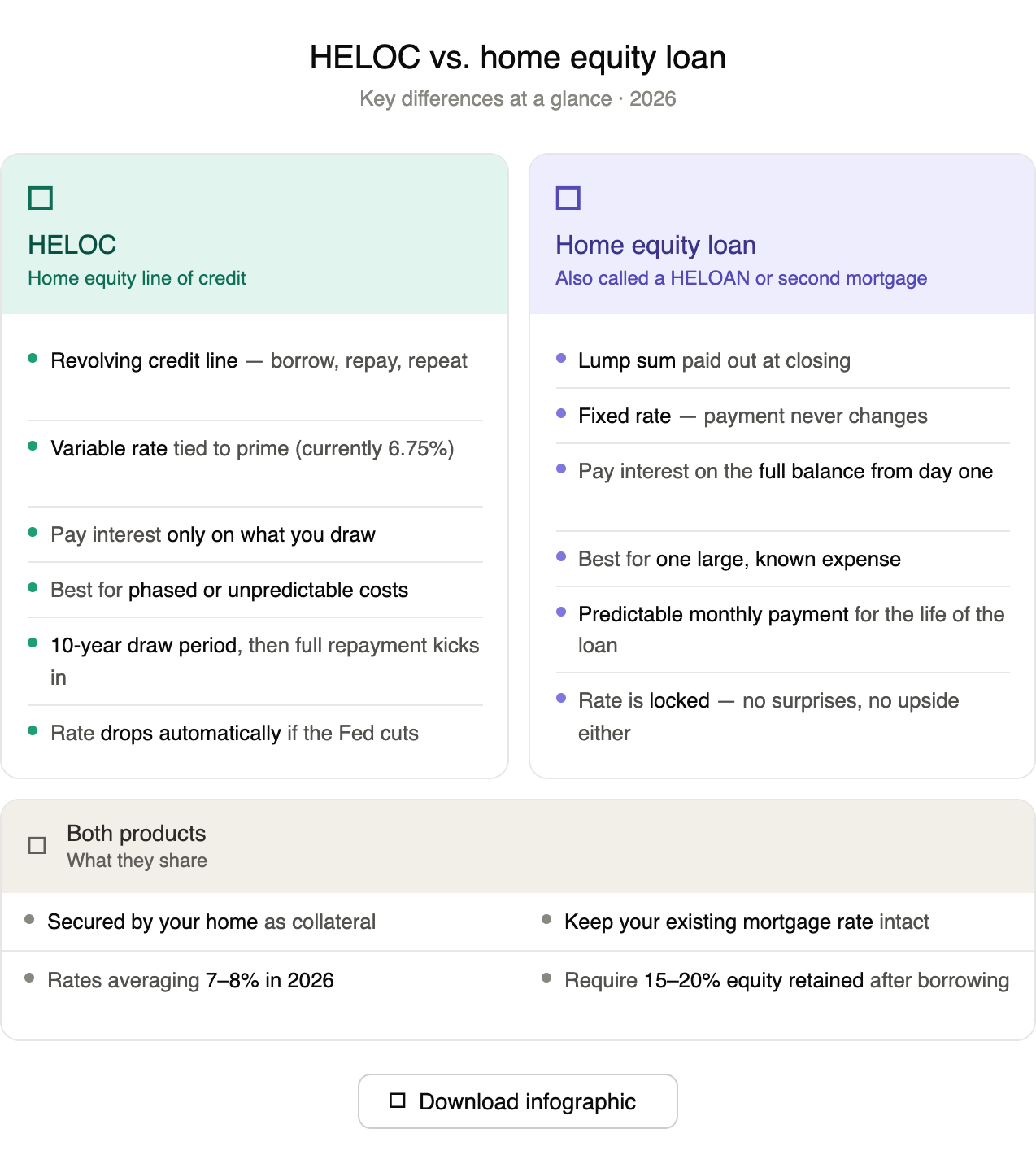

A HELOC — home equity line of credit — is a revolving credit line secured by your home. Think of it like a credit card, except the limit is tied to your equity and the rates are far lower than any card you’ve seen.

Here’s how it works in practice. Your lender approves you for a credit limit, say $80,000. During the draw period — typically 10 years — you can pull money out as you need it, pay it back, and draw again. You only pay interest on what you’ve actually borrowed, not the full limit. That makes a HELOC flexible in a way a home equity loan simply can’t match.

After the draw period ends, you enter the repayment period, which usually runs 20 years. That’s when full principal-and-interest payments kick in. The total loan becomes a 30-year commitment if you’re not careful — something a lot of borrowers miss until they’re deep in.

The catch: HELOC rates are variable. They’re tied to the Wall Street Journal prime rate, which currently sits at 6.75%. Most HELOC rates today fall somewhere between 7% and 9%, depending on your credit and how much equity you have. If the Fed cuts rates — which analysts are forecasting for later in 2026 — your HELOC payment drops automatically. If rates climb, it goes the other way just as fast.

One client I worked with used a HELOC to fund a phased kitchen remodel: a $15,000 deposit upfront, $20,000 for cabinets two months later, then the rest for finishes and punch-list items. She paid interest only on what she’d drawn at each stage. A home equity loan would have had her paying interest on the full $70,000 from day one.

How a home equity loan (HELOAN) works

A home equity loan, sometimes called a HELOAN, is exactly what it sounds like: a loan. You apply, get approved for a specific amount, and receive that money as a lump sum at closing. Then you repay it in fixed monthly payments at a fixed interest rate just like a second mortgage.

That predictability is the whole point. You know your payment on day one and it never changes. No Fed decisions to worry about. No surprises when you open your statement. For people who need budget certainty, that consistency is worth a lot.

Home equity loan rates in 2026 are averaging around 7.36% to 8.54%, according to Curinos data from June 2026. Slightly higher than HELOC rates right now, but the spread is close — and the rate stability you get in return can absolutely be worth that small premium.

The trade-off is flexibility. You get one shot. If your project comes in under budget, you’ve still borrowed the full amount and you’re paying interest on every dollar. If costs run higher than expected, you’ll need to apply for more financing separately.

I’ve seen this play out differently for different borrowers. One couple came in for a $50,000 bathroom remodel — fixed contractor bid, fixed timeline. A home equity loan was the clear call. Another borrower came in for a “full home renovation,” couldn’t give me a firm number, and wanted to start with the kitchen and see where things went. That person needed a HELOC.

HELOC vs. home equity loan: side by side

Here’s how the two products compare across the factors that actually matter:

- How you receive funds: HELOC — draw as needed; Home equity loan — lump sum at closing

- Interest rate type: HELOC — variable (tied to prime); Home equity loan — fixed

- What you pay interest on: HELOC — only what you draw; Home equity loan — full balance from day one

- Monthly payment: HELOC — fluctuates with rate and draw amount; Home equity loan — fixed for the life of the loan

- Draw period: HELOC — yes, typically 10 years; Home equity loan — no draw period, funded at closing

- Best for: HELOC — phased or uncertain costs; Home equity loan — one large, defined expense

- Rate risk: HELOC — yes, rates can rise; Home equity loan — none once you lock

Both products sit behind your first mortgage. Neither one changes your existing rate. And both use your home as collateral — a point we’ll come back to.

What rates look like right now

As of mid-2026, HELOC rates average around 7.23% to 9.39% and home equity loan rates average around 7.36% to 8.54%, per Curinos data. The gap between them is unusually narrow right now — which makes the decision less about chasing the lower rate and more about which structure actually fits your borrowing pattern.

A few things worth knowing about the rate environment:

- The Fed is expected to cut rates at least a couple more times in 2026, which would lower HELOC rates automatically for existing borrowers

- Some lenders are offering introductory HELOC rates as low as 5.99% for the first 12 months — but those convert to fully indexed variable rates after the promo period ends. Compare the fully indexed rate, not the teaser

- A home equity loan locks you in today. That’s a guarantee against rate increases, but also means you won’t benefit from future cuts without refinancing

The honest answer is that the rate difference between a HELOC vs. home equity loan in 2026 is small enough that it shouldn’t drive the decision by itself. Structure matters more than the number on the rate sheet.

When a HELOC is the better choice

Choose a HELOC when two or more of these are true:

- Your project will come in stages or phases over months

- You don’t know the exact total cost yet

- You want flexibility to draw, repay, and draw again

- You’re comfortable with a variable rate and have room in your budget if it rises

- You want to keep a credit line available after the project for emergencies

Home renovations are the classic HELOC use case — especially when you’re working with contractors across multiple stages. You only pay interest on what you’ve actually drawn, which saves real money on a multi-phase project compared to sitting on a lump sum for months.

Debt consolidation can also work well with a HELOC if you’re paying off balances in chunks over time and your income is stable enough to absorb rate movement.

When a home equity loan is the better choice

Choose a home equity loan when:

- You know exactly how much you need — fixed contractor bid, specific debt payoff total, defined project cost

- You want a payment that never changes so you can budget around it

- You’re not comfortable with variable rates or the possibility of payment increases

- You want to pay down principal from day one rather than making interest-only payments

Debt consolidation is actually one of the strongest use cases for a home equity loan. Replacing a 19% credit card rate with a fixed 7.5% rate is significant savings — and the fixed payment structure makes it nearly impossible to just “let the balance float,” which is the main trap with revolving credit.

A client came to me carrying $38,000 across four credit cards. We used a home equity loan to wipe them out and cut her monthly payments by over $600. The fixed structure made sure she couldn’t re-draw the balance the way she could with a HELOC.

A 3-question framework to make the call

Still not sure which direction to go? Work through these three questions:

- Do I know exactly what I need to borrow? If yes — lean toward a home equity loan. If the number is fuzzy or phased — lean toward a HELOC.

- Can my budget handle a payment increase? If a 2% rate jump on your HELOC balance would create real strain, a fixed home equity loan removes that risk entirely.

- Do I need ongoing access, or a one-time funding? If you want a credit line you can tap, repay, and draw from again — that’s a HELOC. If you need money once and want to be done with it — that’s a home equity loan.

Most borrowers can answer all three in under two minutes. The answer usually points clearly in one direction.

The risk both products share

Both a HELOC and a home equity loan use your home as collateral. That’s not a reason to avoid them — but it’s a reason to be honest about what you’re using the money for and what your repayment plan looks like before you sign.

If you miss payments, foreclosure is a real possibility. These are second mortgages, not personal loans. The lower rate comes with that tradeoff.

Lenders typically require you to retain 10% to 15% equity after borrowing — meaning most cap your combined loan-to-value (CLTV) at 80% to 85%. Some go as high as 90%. The average HELOC credit limit nationwide is around $129,000, though the actual number you qualify for depends on your home’s value, what you owe, and your credit profile.

Borrow what you need. Have a payoff plan. And if you’re using home equity to pay off consumer debt, make sure you’re also addressing whatever created those balances in the first place — otherwise you risk ending up with both the debt and a loan secured by your home.

What about a cash-out refinance?

A HELOC and a home equity loan aren’t the only ways to tap your equity. There’s a third option worth knowing about: the cash-out refinance. It works differently from both — and in 2026, it’s the right call for fewer homeowners than it used to be.

Here’s how it works. A cash-out refinance replaces your existing mortgage entirely with a new, larger loan. The difference between what you owed and the new loan amount is paid out to you in cash at closing. One loan, one payment, one rate — clean and simple.

The catch is significant right now. Millions of homeowners locked in mortgage rates of 2% to 4% between 2020 and 2022. A cash-out refinance would replace that rate with whatever today’s market offers — currently hovering above 6.5% to 7%. On a $300,000 mortgage, that rate jump can add $600 or more to your monthly payment. That’s a steep price for accessing cash.

That’s exactly why HELOCs and home equity loans have surged in popularity. Both sit behind your first mortgage as second liens — meaning your low rate stays completely untouched. You only pay the higher rate on the new money, not your entire balance.

So when does a cash-out refinance actually make sense in 2026? A few scenarios:

- Your current rate is already at or above today’s rates. If you bought or refinanced at 6.5% or higher, replacing it doesn’t cost you much — and you simplify down to one loan.

- You need to borrow a very large amount. Cash-out refis typically allow higher loan amounts than second liens, since they’re based on your total home value rather than just your equity above the first mortgage.

- You want to consolidate your first and second mortgage. If you already have a home equity loan or HELOC and want to roll everything into one payment, a refi can make that happen.

- Rates drop significantly. If mortgage rates fall to a level close to or below your existing rate, a cash-out refi becomes worth revisiting.

RELATED: Read about our 95% Cash-Out Refinance Mortgage

One client came to me with a 6.75% first mortgage from late 2023 and needed $80,000 for a full home addition. For him, a cash-out refinance made sense — the rate difference was minimal, and simplifying to one payment was worth it. Compare that to the client with a 2.875% rate who needed $60,000 for a kitchen remodel. She used a HELOC without hesitation. Same need, completely different answer.

The bottom line: if you have a rate below 5%, protect it. A HELOC or home equity loan almost certainly costs you less in the long run than giving up that rate to do a cash-out refi. If your rate is already in the mid-to-high 6s or above, the calculus changes — and a cash-out refinance deserves a spot in the conversation.

Ready to find out what you qualify for?

Three solid options, one right answer — and it depends entirely on your rate, your equity, and what you need the money for. A HELOC gives you flexibility. A home equity loan gives you certainty. A cash-out refinance simplifies everything into one loan, but only makes sense if the rate tradeoff works in your favor.

In 2026, with rates near recent lows and homeowners holding record amounts of equity, it’s worth getting real numbers before you decide. Rates vary significantly from lender to lender — even a half-point difference on a $100,000 loan adds up fast over 10 or 20 years.

Talk to our team today to compare your options and see what you qualify for. No hard credit pull to get started.