When buying a home, your credit score is an important factor in your home loan approval. It is important to know what is on your credit and what credit score you have when applying for a mortgage.

While, the exact scoring models are proprietary and not released by the credit bureaus to the public, credit experts have determined the weight of each factor that determines your credit score.

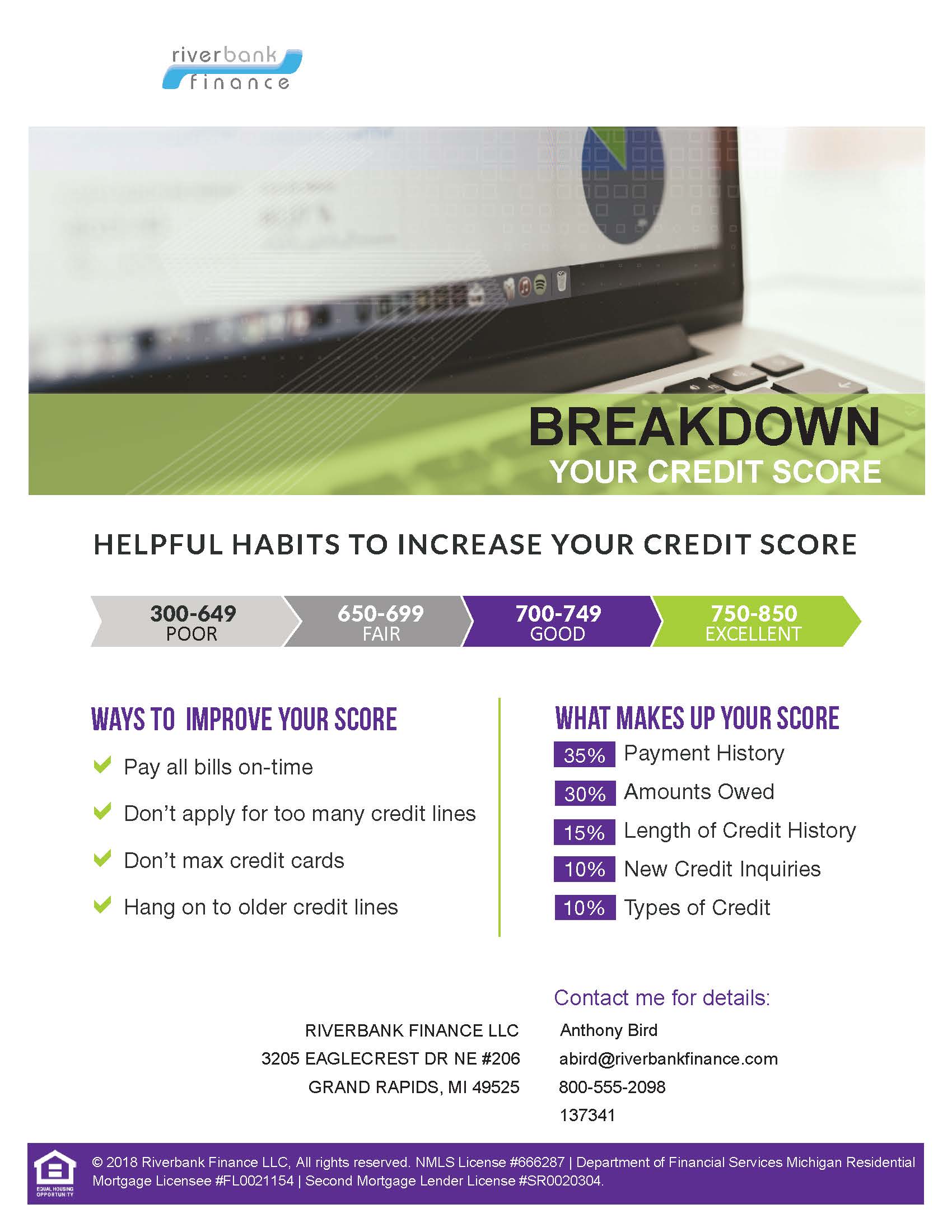

Related: Buying a home with Bad Credit may be possible with FHA Home Loans. We accept applications down to a 580 credit score!

What Makes up your Credit Score

Payment History

Paying your bills on time is the most important factor for your credit score. Weighted at 35% of the total score, paying bills late can devastate your credit rating.

Amounts Owed

Credit to Debt ratios are the second most important factor which is weighted at 30% of the overall score. The good news about this is that it is a quick and easy fix to improve your credit scores. For example, if you have a credit card with a $500.00 limit and you owe $490.00, it is essentially “Maxed Out” which reflects poorly on your credit rating. Paying down this debt to under 30% of the limit ( $150 or less in this example) would boost your scores quickly!

Length of Credit History

The length of time you have had accounts open is the next rating factor. At 15% of the credit rating, the credit bureaus know that maintaining long credit relationship with banks and lenders proves that you are a good credit risk and positively affects your score. For this reason, it is important to keep old credit lines open even if you are not utilizing them.

New Credit Inquiries

Having your credit pulled is an necessary evil when applying for a mortgage. What is not necessary is having it pulled by 10 different institutions for different credit types. If you apply for credit cards, auto loans, and mortgages over a short period of time, your credit rating may drop.

Types of Credit

The final major category that determines your credit score is the types of credit that you hold. Long term investments such as a mortgage can positively impact your credit. If you only have revolving credit such as credit cards, your credit depth is shallow and may not give you the highest credit scores possible.

Click here to Download Our Credit Tip Flyer!

How to Improve your Credit Score

There are simple techniques to improving your credit scores. It is important to monitor your credit from time to time and make sure all of the information is accurate. If there are errors, you can dispute the information directly with the bureaus to have it corrected. It is not suggested that you do this before or during the mortgage process as it may cause delays.

Additionally, paying down revolving account balances can quickly boost your credit scores. While there are no magical fixes to your credit, there are several best practices that you should do to increase your credit score.

Tips to Improve your Credit Rating

- Correct inaccuracies on your credit

- Pay all your bills on time.

- Do not apply for too many lines of credit.

- Do not max out credit cards.

- Keep older credit lines open.

Contact a mortgage expert today by calling us at 1-800-555-2098 or simply apply online below. We are happy to help!