Home loans for nurses? You may have heard about doctor loans but most people do not know that there is a zero down mortgage for nurses. Nurses spend their careers caring for others, but buying a home can feel anything but caring. Student loan debt, variable income, long shifts, limited time, and saving for a large down payment can make the mortgage process stressful.

The good news is that specialized home loans for nurses, including medical professional mortgage options, may offer flexible financing and even 100% financing for qualified borrowers. This guide explains how home loans for nurses work, who may qualify, what benefits are available, and how to get started with confidence.

What Are Home Loans for Nurses?

Home loans for nurses are special mortgage options built for healthcare pros. They tend to come with more flexible terms than your average loan. Think of them as a thank-you for the long shifts and the lives you touch.

Who qualifies? Quite a few folks, actually. Registered nurses. Nurse practitioners. Travel nurses. Nurse midwives. And plenty of other medical professionals. If you have one of the following medical licenses, you may be eligible: Registered Nurse (RN), Nurse Midwife (APRN), Nurse Practitioner (NP), Nurse Anesthetist (CRNA).

The perks can be pretty nice. No down payment required. Easier debt-to-income guidelines where we can waive your student loan payments. Competitive interest rates. No Private mortgage insurance. Just keep in mind… not all will qualify so it is important to talk to a loan officer to review what is best for your situation.

100% Financing Home Loans for Nurses: How They Work

Here’s the headline: 100% financing means the lender may cover the full price of the home. No down payment. Zero. That’s huge when you’re trying to buy without draining your savings.

But let’s be real. You’ll likely still need cash for a few things. Closing costs. Prepaid expenses. Inspections. Other odds and ends. Unless some assistance program steps in to help.

So what gets you approved? Lenders look at your credit score, income, and how long you’ve worked. Your debt-to-income ratio. The type of property. The loan amount. Where the home is. And the lender’s own rules. A lot of moving parts, but nothing you can’t handle.

Benefits of a Medical Professional Mortgage for Nurses

The biggest win? You may buy sooner. No need to spend years scraping together a down payment. I once worked with a nurse who’d been renting for a decade, convinced she’d never afford a place. Turns out she qualified faster than she expected. The relief on her face? Unforgettable.

The benefits stack up nicely:

- 100% financing

- Low down payment alternatives

- Competitive mortgage rates

- Flexible underwriting

- Higher loan limits

- No PMI

Why do lenders roll out the red carpet? Simple. Nurses are always in demand. Strong earning potential. Solid career growth. From a lender’s view, that’s a safe bet.

Nurse Home Buying Program Options to Consider

You’ve got choices. More than you might think. Medical professional mortgages. Conventional loans. FHA loans. VA loans. USDA loans. State housing programs. Grants. Down payment assistance.

Some fit certain situations better. VA loans? Great for military nurses or their spouses. USDA loans? Worth a look if you’re buying in a rural or suburban spot.

FHA loans can help if your credit isn’t perfect. And medical professional mortgages shine when you want low or no money down. The trick is matching the loan to your life.

Home Buying Assistance for Nurses

Free money? Well, sometimes. Assistance comes in many flavors. Down payment help. Closing cost help. Grants. Tax credits. Employer housing benefits. Community hero programs.

Eligibility has strings, though. It may hinge on income limits. Location. Whether you’re a first-time buyer. Occupancy rules. Your credit and debt.

Here’s the part people skip… read the fine print. Assistance might be a grant, a forgivable loan, a deferred-payment loan, or a tax credit. Some you pay back. Some you don’t. Know which one you’re getting before you sign.

Home Loans for Nurse Practitioners

NPs, this one’s for you. Your advanced credentials work in your favor. Strong income potential. Steady demand. Lenders notice.

When reviewing your application, they may dig into salary, bonuses, overtime, contract income, self-employment income, or practice income. The more clearly you document it, the smoother things go.

And those student loans from your advanced degree? Don’t panic. NP mortgage loans may help you buy with less cash upfront, even with that balance hanging around.

Nurse Practitioner Mortgage Loans: What Makes Them Different?

These loans are tailored to your financial reality. Built for NPs and advanced practice nurses, not a one-size-fits-all crowd.

The features can be generous:

- Low down payment options

- 100% financing

- Flexible student loan treatment

- Competitive rates

- Higher borrowing capacity, depending on income and credit

One word of caution. Don’t fall for a flashy rate alone. Look deeper. Compare fees, APR, discount points, mortgage insurance, closing costs, and prepayment terms. The lowest advertised rate isn’t always the best deal. Sometimes it’s a magician’s trick… pretty distraction, hidden cost.

Low Mortgage Rates for Nurses: How to Qualify

Rates depend on two things. The market. And you.

You can’t control the market. But your qualifications? That’s your lane. Credit score, down payment, loan type, debt-to-income ratio, property type, loan term, rate lock period… they all push your rate up or down.

Want a better number? Here’s how to nudge things your way:

- Strengthen your credit

- Knock out high-interest debt

- Compare lenders (always)

- Consider a rate buydown

- Ask about healthcare professional pricing

That last one matters. A lot of nurses never ask. So they never find out.

Mortgage Options for Travel Nurses

Travel nurses, your income is… complicated. Contracts. Stipends. Housing allowances. Overtime. Sometimes multiple employers. Lenders see that and ask a million questions.

Be ready to hand over a stack of paperwork. Contracts. Pay stubs. W-2s. 1099s. Tax returns. Employment history. Assignment records. Bank statements. Yeah, it’s a lot.

My advice? Find a lender who actually gets travel nursing. Then confirm one key thing early: can your stipend income count? That answer can make or break your approval.

Who Qualifies for a Nurse Mortgage Program?

The list of eligible pros is long. RNs. NPs. Travel nurses. LPNs and LVNs. Certified nurse midwives. CRNAs. Physician assistants. Physicians. Dentists. Pharmacists. And more.

The usual requirements look like this:

- Proof of employment

- Professional license or credentials

- Qualifying income

- Acceptable debt-to-income ratio

- Minimum credit score

- Plans to live in the home as your primary residence

Here’s the catch. Every lender does it a little differently. So get pre-approved before you start touring homes. It saves heartbreak later.

Student Loans and Home Loans for Nurses

Let’s talk about the elephant in the room. Student loans. They bump up your monthly obligations and your debt-to-income ratio. That can make approval trickier for most home loans.

But it’s not a dead end. Far from it. Some medical professional mortgages treat deferred loans or income-driven repayment plans more kindly than standard loans do. We may have options to exclude your student loan payments in full to help you qualify for a higher loan amount.

First-Time Homebuyer Tips for Nurses

First home? Exciting and a little terrifying. I get it. Take a breath and start with the basics.

- Review your credit reports

- Estimate a realistic monthly budget

- Compare mortgage options

- Save for closing costs

- Gather income documents early

Then get pre-approved. This step is gold. It tells sellers you’re serious and keeps you shopping within budget. No falling for the dream house you can’t actually afford.

One more thing. Make sure you are taking to loan officers and agents who understand nurse life. Digital applications. Flexible communication. Remote closings. Agents who won’t blink at your 7-on, 7-off schedule. That stuff makes a real difference when you’re running on coffee and three hours of sleep.

How to Apply for a Medical Professional Mortgage

The process isn’t scary once you break it down.

Start here: confirm you qualify as a nurse or healthcare pro. Then take an honest look at your credit, income, debt, and savings.

Next, work through the steps:

- Apply Online

- Talk with a loan officer to get pre-approved

- Shop within your budget

- Submit your documents

- Complete underwriting

- Close on your home

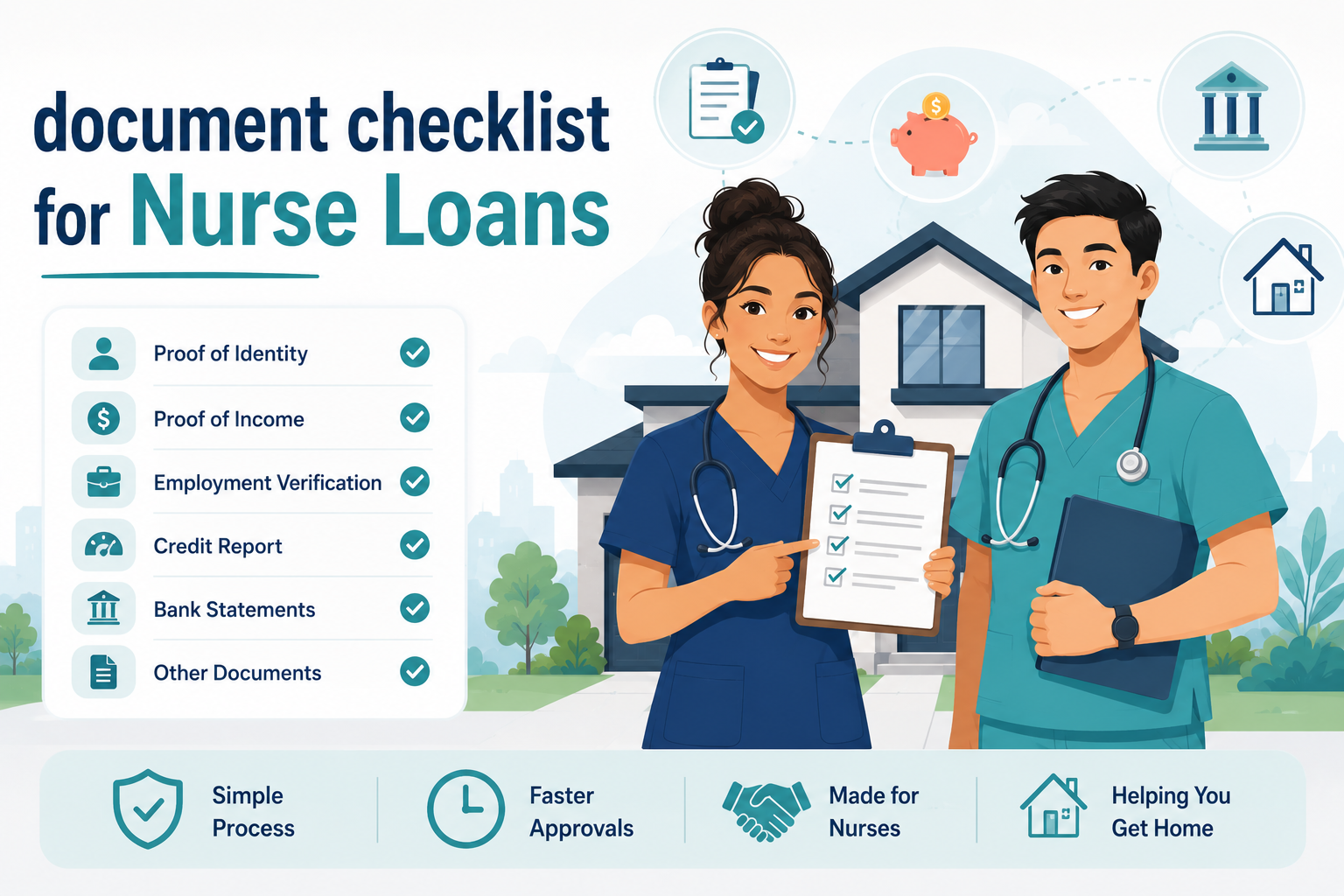

Gather your paperwork ahead of time. You’ll likely need ID, your nursing license, pay stubs, W-2s, tax returns, employment verification, bank statements, student loan statements, and travel nurse contracts if those apply. Pro tip: keep it all in one folder. Future you will say thanks.

100% Financing vs. Low Down Payment: Which Is Better for Nurses?

Great question. And honestly… it depends.

100% financing lets you buy now. No down payment. Your emergency savings stay right where they are. For some nurses, that peace of mind is everything.

But trade-offs exist. A higher monthly payment. More interest over time. Less equity at the start. Sometimes tougher qualification rules.

A low down payment flips the script. It shrinks your loan. Often improves your pricing. And gives you equity from day one.

So what should you do? Compare two loan estimates side by side. See the real numbers. Then decide what fits your goals, not someone else’s.

Common Mistakes Nurses Should Avoid When Buying a Home

I’ve seen good buyers stumble over avoidable stuff. Let’s keep you clear of it.

Don’t assume every nurse mortgage program is the same. They aren’t. Compare rates, fees, and terms before you commit.

And please… before closing, don’t:

- Take on new debt

- Change jobs

- Make large unexplained deposits

At least not without telling your lender first. A surprise can stall your whole loan.

Also, don’t forget the extras. Closing costs. Property taxes. Insurance. Credit hiccups. And documentation for overtime or shift differential income. That income counts, but only if you can prove it.

Questions to Ask Before Choosing a Nurse Home Loan

Don’t be shy. Asking questions is smart, not annoying. Here’s what to put on your list.

Ask if the lender offers home loans for nurses, 100% financing, healthcare worker discounts, reduced fees, or home buying assistance.

Ask who qualifies. Nurse practitioners? Travel nurses? Other healthcare pros? Get specifics.

Then dig into the details. How do they handle student loans, overtime, bonus pay, shift differentials, and contract income? What about credit score, mortgage insurance, closing costs, and pre-approval timelines? The more you ask, the fewer surprises later.

Frequently Asked Questions About Home Loans for Nurses

Can nurses get 100% financing on a home?

Yes, eligible nurses may qualify through certain medical professional mortgage programs. It comes down to lender guidelines, income, credit, and where the home is.

Are there special mortgage rates for nurses?

Our nurse home loan offers low rates for nurses and other medical professionals. Usually the nurse mortgage rates are lower than a conventional mortgage.

Do nurse practitioners qualify?

Yes you can be a nurse practitioner (NP) and qualify for our zero down mortgage with no PMI.

Can travel nurses qualify?

Yep. The income paperwork is just trickier. You will need to document stable future income and a history of working as a travel nurse.

Do nurses need a down payment?

Sometimes no, sometimes yes. Some programs offer 100% financing. Others want a low down payment. Either way, closing costs may still pop up.

Can nurses with student loans buy a house?

Absolutely. Student loans don’t automatically block you. Lenders just look at your repayment status, monthly payments, and debt-to-income ratio.

Are Medical professional loans available for Physician Assistants?

Yes you can be a Physician Assistant (PA) and qualify for our zero down mortgage with no PMI.

What is the best home loan for nurses?

There’s no single winner. It depends on your credit, income, savings, location, profession, and goals. Compare medical professional mortgages, FHA, VA, USDA, conventional, and assistance programs. Then pick the one that fits your life.